Discussion: https://www.svb.com/trends-insights/reports/dtc-wine-survey-report-2024/

Silicon Valley Bank’s 2024 Direct-to-Consumer Report presentation tried very hard to gild bad news in silver linings. There was very little positive to be found in the hard data presented. The discussion panel tried their best to say all is not doomed. And while I won’t say the industry is doomed, it is facing some pretty big challenges right now.

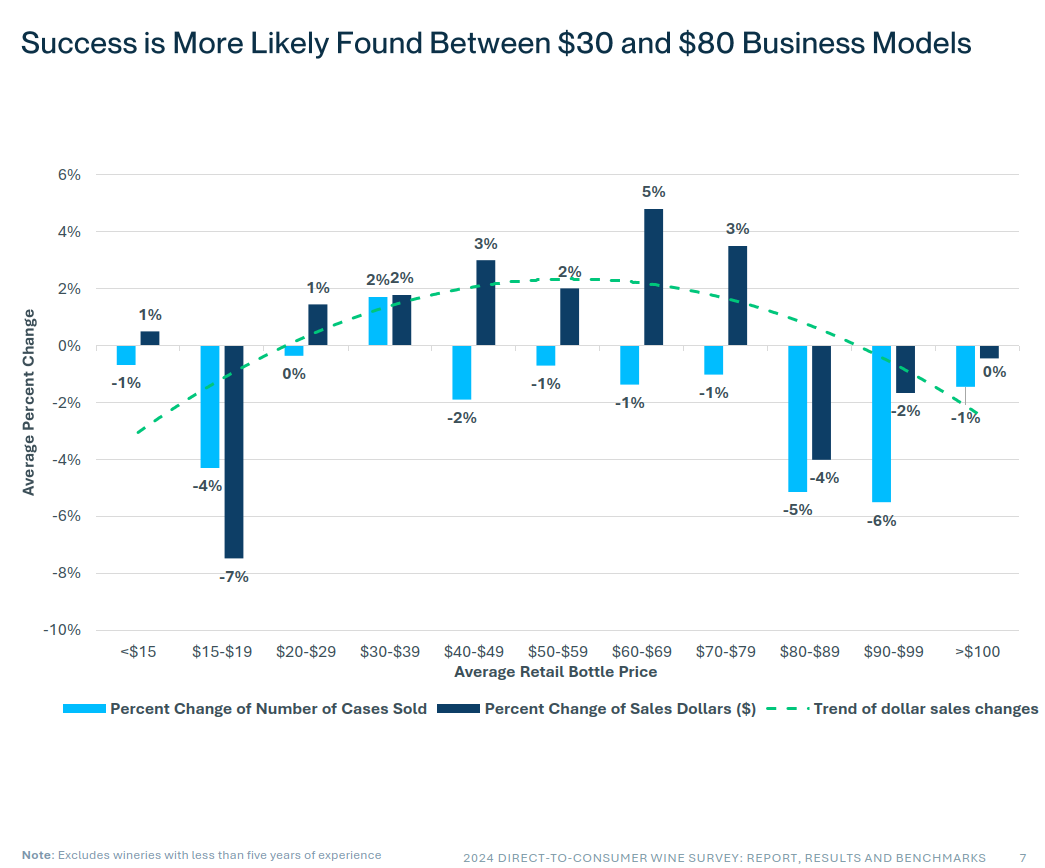

The gilding came in the form of data that shows sales volume is down for the under-$20 SRP wine category, but sales dollars are up for more expensive wines. Only one panelist pointed out that price increases were likely a major driver for that positive data. But the DTC data also showed declines or flat growth in the sales volume of super-premium to ultra-premium priced wines. The usual tropes of generational shifts, competition by other beverages, and overstocking were offered. But this underlying softness in the whole market is what needs to be examined and countered by the industry.

First and foremost is the change in consumer purchasing behavior, no matter what generation they belong to. This is affecting all industries and not just alcoholic beverages. The internet – and Amazon in particular – has taught us to buy what we need when we need it now, i.e., just-in-time (JIT) purchases. Yes, we do stock up on household staples a bit – no one is buying one roll of TP at a time – but when it comes to luxury goods, the impetus to stock up is disappearing.

Furthermore, every company is trying to convert consumers to subscriptions for goods and services. We are seeing a rebellion against this model, starting with the cable companies that priced their poor services higher than what consumers wanted; when options appeared, consumers cut the cable. But consumers are confronted with subscriptions that still have a certain amount of lock-in: internet access, mobile cellular services, some media, PC services, etc., not to mention rent, mortgages, and car payments are all commanding a reoccurring commitment out of personal finances. This dedicated portion of personal budgets exacerbates the desire to only buy what is needed when it is needed or wanted.

Finally, the consumer has more choice than ever. Brand loyalty is tenuous when options are plentiful. Brand loyalty is especially iffy when companies aren’t loyal back. The rise of the big companies that limit market options has especially jaded consumers, as the companies have no motivation to return loyalty when their customers have few options. Big, global, wine corporations only create an illusion of choice but control the vast majority of brands sold in the U.S.

The wine industry has been based on brand loyalty, subscription wine clubs, and buyers stocking up inventories. But these economic changes are not going to change back, especially as younger people grow up with no other purchasing model to compare it to. The future consumer is used to options, JIT ordering and delivery, and consuming what they purchase sooner rather than later.

The panel or the report did not discuss consumer behavior, which seems like a big miss.

Only Rob McMillan mentioned the global, anti-alcohol efforts. Anti-alcohol organizations are using the anti-tobacco playbook and are building a temperance movement via two strategies: regulatory, as witnessed by the World Health Organization announcements, and making alcohol consumption socially unacceptable. If they succeed, and especially with the latter strategy, then alcoholic beverages will continue to decline for generations. This is a substantial threat to the societal and personal benefits of moderate wine drinking – more so than the generational shift the industry has been wringing its hands over for the last ten years.

Last, the panel’s discussion about pricing was problematic. While tasting room fees certainly have room for adjustment (or discounting), there is less flexibility with wine made by most small and mid-sized wineries. As a grower myself, in the last four years costs for land, taxes, insurance, labor, fuel, chemicals, etc., have all had substantial increases … along with the cost of borrowing. None of these costs – except possibly the cost of borrowing – will go back down without a serious shock to the economy. Small vineyard growers do not have the economies of scale to adjust for the recent disruptions from the pandemic and inflation. Likewise, wineries have had increases in their costs, including glass, labels, winemaking materials, barrels, etc. Costs are up, and will stay up, at least in the most popular wine-growing regions.

Therefore, at least in regards to West Coast wines, prices will stay up. Only the biggest wineries will be able to increase margins and adjust costs by blending established vineyards with cheaper imports. Small and mid-sized wineries have no choice but to pass higher costs to customers. We as an industry must do better in convincing our customers that the value of our wines are still there, as the price increases contain intrinsic values such as fair pay, sustainability, and supporting local and family agriculture.

McMillan acknowledged that there are, in reality, two distinct wine industries. The “premium” wines (in industry parlance super-premium to ultra-premium priced wines made by small and mid-sized wineries) and the big, global, corporate wineries (Big Wine). Those two, very different industries extend through the three-tier sales channel, as only the large, multi-state, wholesale distributors can work successfully with Big Wine, while smaller wholesale distributors struggle to compete with their portfolios of premium brands. Likewise, the national big box, chain retailers such as Total Beverage or Sam’s Club get favorable treatment from multi-state wholesale distributors and global wineries, putting extreme pressure on small, independent or regional wine retailers. Big Wine – producers, distributors, and chain retail – can work on thinner margins and have the staff to reach more trade outlets and store shelves, providing consumers consistency, availability, and pricing.

As an aside, that’s why the suggestion by the panel to secure wholesale distribution in states where you have clusters of DTC customers made me laugh; what winery wouldn’t naturally do so? But the suggestion completely disregarded the realities of the two industries and the wholesale market: the difficulty in finding distribution as options shrink due to M&A, the loss of even more margin, the cost of compliance, the cost of supporting a market, and more. Wholesale distribution is an undertaking that most small wineries cannot afford – or do easily.

McMillan’s lamented WineRAMP solution was and is not the answer for today’s woes, as that did not factor in the two distinct wine industries. Generic category advertising did not work in the past, and is even more outdated in today’s media market. If there is to be success, cooperation and effort must be more focused on what premium brands need, not what Big Wine wants. Big Wine will benefit from the success of any industry marketing. It doesn’t work the other way for premium brands. This isn’t to create a rift between premium brands and Big Wine, but to point out that the needs of premium brands are not being recognized as different from Big Wine’s needs.

The panel echoed a current, popular, industry response to all of this negative news: yep, some are going to go out of business. Focus on being one of the successful ones instead. Easy to say, hard to do. Especially hard to do if you are small or mid-sized, and economic forces are against you.

The DTC channel has the ability to be the more successful strategy in the changing market landscape. One-to-one communications make for more of a lasting impression with consumers. Wineries have the chance to promote their brands, their wines, moderate consumption, and a balanced lifestyle through DTC sales. Adjustments to DTC sales programs need to recognize that purchases will be smaller, hopefully more frequent, and that more interaction and loyalty be offered in return for consumers’ loyalty and support.

This is so much more than “telling your brand story,” “meeting your customers where they are,” and “guiding them on their customer journey” – clichés offered by the panel. It is examining your product portfolio, changing your sales strategies to the newer market and economic trends, and being more adaptable in your marketing messaging based on audience, occasion, and channel.

Premium brands are not going to be able to tackle the bigger issues facing the industry alone, however. Cooperation and effort must be made to combat anti-alcohol efforts, poor regulations, and industry consolidation. Working with industry organizations, regional wine-growing organizations must do more than promote their region; they must be a voice for a more competitive and expansive market, actively promote moderate drinking, and build more diverse sales and marketing channels.

They also must make the case to outlet buyers and consumers that the prices for their members’ wines are a value. The quality is there. The prices deliver the goods, fairly support the families and workers making them, and consumers will find satisfaction and value in them. Wine provides pleasure and enrichment in ways that no other beverage can.